Brokered CDs and Credit Union Share Certificates Underwriting

Help grow your business with our vast client network.

Leverage Fidelity's diverse relationships to raise deposits through brokered certificates of deposit (CD) and credit union share certificates (CUSC) underwriting. In 2025, we helped over 450+ issuers raise $142B+ in deposits, supported by seamless investor access via Fidelity.com

and our mobile app.1

Reliable and cost-effective funding

Financial institutions participate in retail CD and CUSC programs because they are a cost-effective and flexible funding mechanism that can complement their other funding options.

Flexible CD and CUSC structures

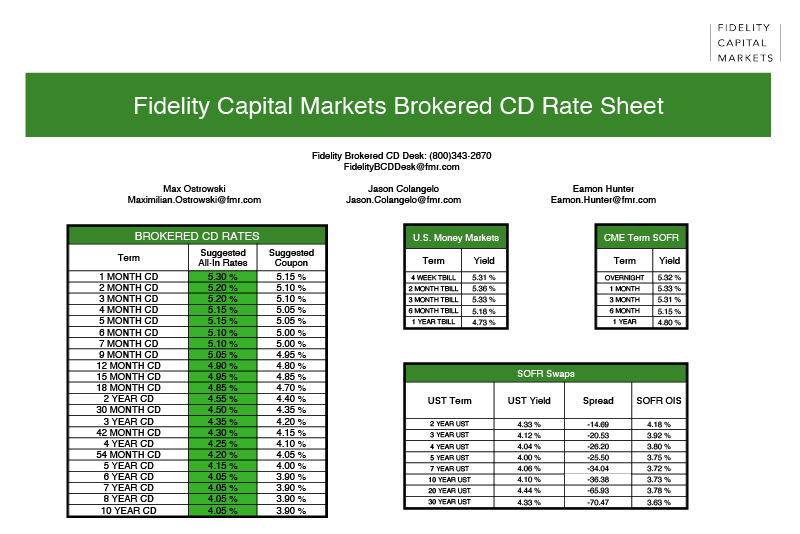

Retail CDs and CUSCs are issued in various terms and structures. They are issued on a continuous or periodic basis to help meet a wide range of financing requirements.

Operational and regulatory benefits of issuing brokered CDs and CUSCs

- Master certificates—Retail CDs and CUSCs are insured (CDs by the FDIC and CUSCs by the NCUA) time deposits issued to holders in "book-entry" form only. Only one master certificate is required for each issue regardless of the number of depositors purchasing the issue or the amount raised by the financial institution.

- Custodian—The financial institution makes principal and interest payments to the Depository Trust Company (DTC).2 DTC is responsible for passing the principal and interest to the broker-dealers. The broker-dealer is responsible for passing the correct amount of principal and interest to the owners of the Certificates.

- Regulatory requirements—Bank issuers must be classified as either "Well Capitalized" or "Adequately Capitalized," and have been granted a waiver from the FDIC to accept brokered deposits. Credit union issuers must be federally insured by the NCUA.

- Ease of administration—Principal and interest payments can be aggregated on payment dates and submitted to DTC in one transaction. Closing documents for CDs can be signed electronically via DTC's ECERT program.

- Recordkeeping—Broker-dealers are responsible for maintenance of all depositor records and tax reporting information, and provide depositors with confirmation statements, disclosure documents, and periodic account statements. Tax documents are provided directly to depositors and to state and federal taxing authorities by broker-dealers.

Access retail, advisor, and institutional distribution to reach investors nationwide without incurring marketing fees

- Source: Fidelity Investments 2025 Annual Report.

Want to know more?

Contact our specialists to discuss underwriting strategies for your firm.

800.343.2760 or FidelityBCDDesk@fmr.com

- Fidelity Capital Markets unaudited data, as of 12/31/25.

- Depository Trust Company (DTC) is a member of the U.S. Federal Reserve System, a limited-purpose trust company under New York State banking law and a registered clearing agency with the Securities and Exchange Commission. The master certificates are held by DTC for the bank.

Intended for institutional investor use only. Not authorized for distribution to the public as sales material in any form.

Investing in brokered CDs is like investing in bank CDs in that investors agree to place their funds with the issuing bank for the term of the CD, and the CD earns interest at a specified rate. It differs in that brokered CDs may be sold prior to maturity and, in turn, investors may also buy brokered CDs on the secondary market. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. If sold prior to maturity, CDs may be sold on the secondary market, subject to market conditions.

Fidelity offers new-issue brokered CDs that carry FDIC insurance coverage. National Financial Services LLC and/or the Depository Trust Company (DTC) maintains the records of each brokered depositor in accordance with applicable requirements of the FDIC and brokerage agreements with the CD underwriters. The Federal Deposit Insurance Corporation (FDIC) insures CDs for principal and accrued interest up to $250,000 per issuer. In some cases, CDs may be purchased on the secondary market at a price that reflects a premium to their principal value. This premium is ineligible for FDIC insurance. Additional information can be found on the FDIC website at www.fdic.gov.

Brokered credit union share certificates (CUSC) are issued by a credit union to brokerage firms for them to sell to their investors. Instead of paying interest like banks, credit unions distribute earnings in the form of dividends if approved by the credit union board. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. If sold prior to maturity, CUSCs cannot be sold on the secondary market.

Fidelity offers new-issue CUSCs that carry National Credit Union Administration (NCUA) coverage. National Financial Services LLC and/or the Depository Trust Company (DTC) maintains the records of each brokered depositor in accordance with applicable requirements of the NCUA and brokerage agreements with the CUSC underwriters. The NCUA insures CUSCs up to $250,000 per issuer. Additional information can be found on the NCUA website at www.ncua.gov.

Fidelity Brokerage and Fidelity Wealth offer retail products and services to individual retail accounts. These entities are a division of Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917.

Fidelity Investments® provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.